An Innovative ETFs Solution based on Core- Satellite Framework

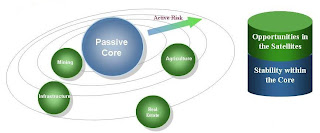

Slide 2I recently implement a core/satellite approach to combine “core”, or diversifying asset class investments, with “satellites” that seek outperformance, aiming to create a dynamic balance between a strong foundation based on diversified asset allocation and opportunities for risk-controlled, enhanced performance.

Core/Satellite delivers the best of both worlds. Passive core investments gives the investor a low cost , tax effective and diversified portfolio, while active satellite exposures gives potential for enhanced returns. The core component of the portfolio is attuned to the investor’s long-term strategic aims, comprising assets that reflect the investor’s appetite for risk. The risk and return are optimally balanced in line with the investment goals of the investor. At the same time, we can implement tactical calls efficiently within the satellite component of the portfolio, which provides the opportunity to pursue shorter-term market-driven investment ideas.

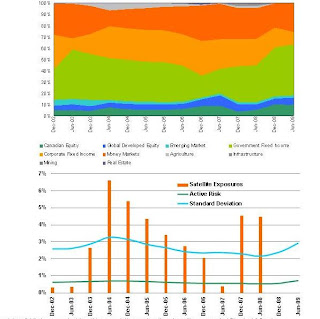

The following chart shows the historical asset allocation and active risk exposures.

The following chart shows the historical asset allocation and active risk exposures.